To receive consistent income from the SCHD ETF, investors can use automatic Dividend Reinvestment Plans (DRIP) or reinvestment of dividends manually. DRIP is like reinvesting dividends automatically into further SCHD shares, compounding the returns with little effort required. Manual reinvestment gives you timing (you can wait for the dip to happen) and diversion flexibility on dividends, which is helpful for advanced strategies or portfolio rebalancing. Both have unique strengths and weaknesses, tax considerations, and set-up procedures. This guide offers step-by-step instructions, real examples, and thought-provoking commentary to enable you to implement and make the most of your SCHD dividend reinvestment plan confidently.

SCHD Dividend Reinvestment: Core Concepts and Income Potential

How SCHD ETF Dividends Work?

- SCHD quarterly pays dividends, depending on the performance of its high-quality U.S. dividend-paying stocks.

- Investors can receive these dividends as cash or reinvest them for compounding growth.

- If you want to understand the basics and structure of this fund, this SCHD ETF guide breaks it down in plain language.

If you want to watch your money grow over the long term, reinvesting dividends is a must. Compounding means that your money can earn more money—each new share you buy with dividends will earn its own dividends next quarter. As time passes, this snowball can turn small payments into big growth in your portfolio.

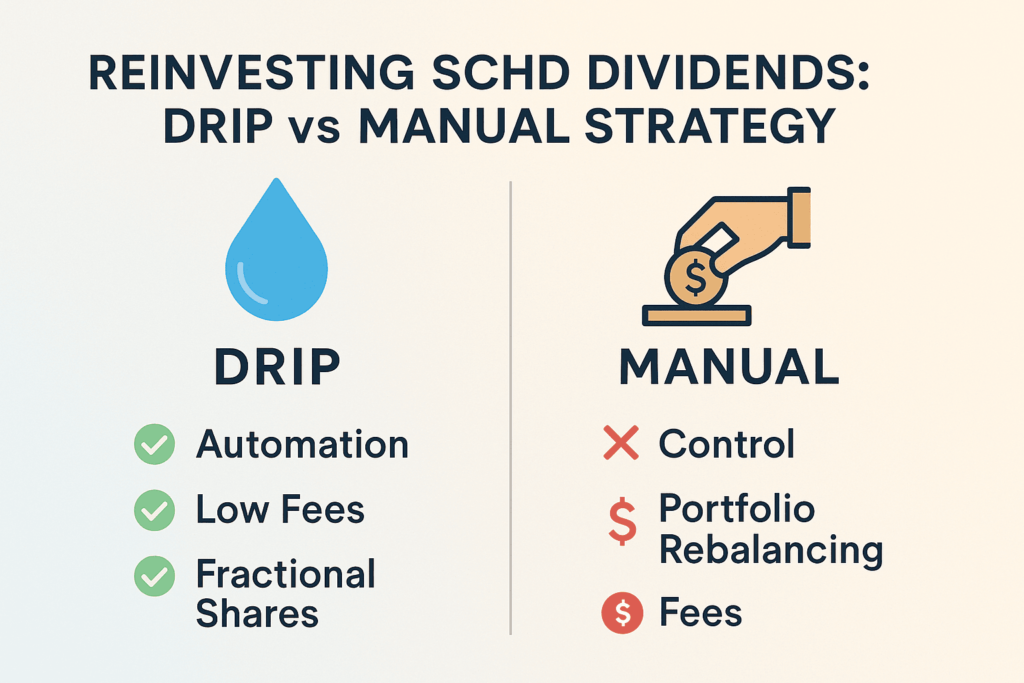

DRIP vs Manual Reinvestment: Key Differences

DRIP (Dividend Reinvestment Plan):

- Your broker buys additional SCHD automatically with each dividend, in fractional shares if needed.

- No commissions on most of the popular brokers.

- You don’t need to lift a finger—set it and forget it.

Manual Reinvestment:

- You receive a cash dividend, then deliberately decide what to do with it.

- Invest in the SCHD, another ETF, or even an alternate stock.

- More flexibility, but you do have to take action and potentially pay trading fees (though most brokers are now commission-free).

Alright, if you want maximum compounding with minimal hassle, DRIP is your hassle-free option. But if you desire control—timing, allocation, or diversification—manual reinvestment is your strong advantage.

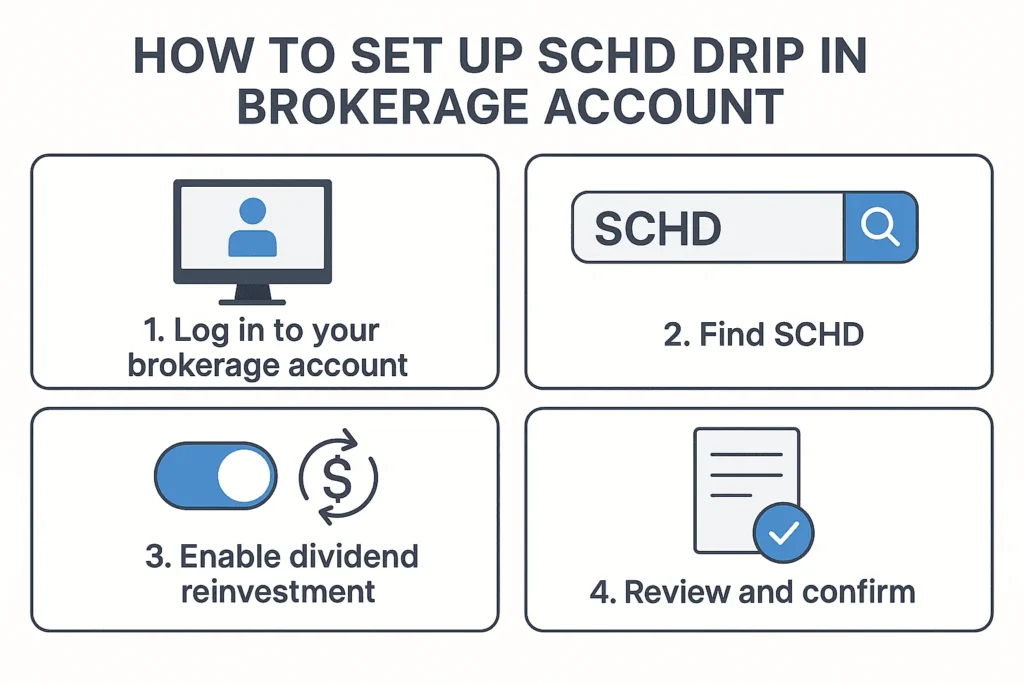

Setting Up SCHD DRIP: Step-by-Step Guide

How to Enable DRIP for SCHD

- Go to your brokerage account (any provider like Charles Schwab, Fidelity, Vanguard).

- Find your SCHD position and choose “Dividend Reinvestment” or “Enroll in DRIP.”

- Confirm enrollment; dividends will now automatically reinvest in SCHD, including fractional shares.

- No commission or fees are charged for DRIP on large U.S. brokerages.

Fixing and Customization

- Turn off or modify DRIP by going back to your accounts settings and choosing “Receive Dividends as Cash.”

- Few brokerages may permit you to tailor DRIP choices for certain holdings.

If you want a set-and-forget approach, this is really very promising. You’ll never miss a reinvestment period, and your portfolio grows away behind the scenes.

Manual Reinvestment for SCHD: Process and Strategy

Executing Manual Dividend Reinvestment

- After receiving SCHD dividends as cash, you can manually purchase SCHD or other investments.

- Manual reinvestment allows you to:

- Time your purchases (buy on market dips).

- Allocate dividends to underweighted assets for portfolio rebalancing.

- Invest in other securities for diversification.

Practical Steps

- Check your account for dividend credits (usually quarterly).

- Place a buy order for SCHD or your chosen security.

- Don’t forget to account for settlement periods and prospective trading commissions, although most brokers have since included commission-free ETF trading.

Manual reinvestment offers you flexibility, but with discipline. If you had money lying around idle or bought your stuff at the incorrect times, you’d be losing the power of compounding. But for those who enjoy fiddling and tuning, this may be worth the while.

DRIP vs Manual Reinvestment: Pros, Cons, and Real-World Examples

| Feature | DRIP (Automatic) | Manual Reinvestment |

|---|---|---|

| Convenience | Fully automatic; set-and-forget | Requires active management |

| Control | No control over timing or price | Full control over timing and allocation |

| Fees | Usually no commissions or fees | May incur commissions (rare with ETFs) |

| Fractional Shares | Supports fractional shares | Depends on broker |

| Portfolio Rebalancing | Not possible—reinvests in SCHD only | Can rebalance or diversify |

| Tax Reporting | Same as cash dividends; reported on 1099-DIV | Same as DRIP |

| Compounding Effect | Maximized via automatic reinvestment | Depends on investor discipline |

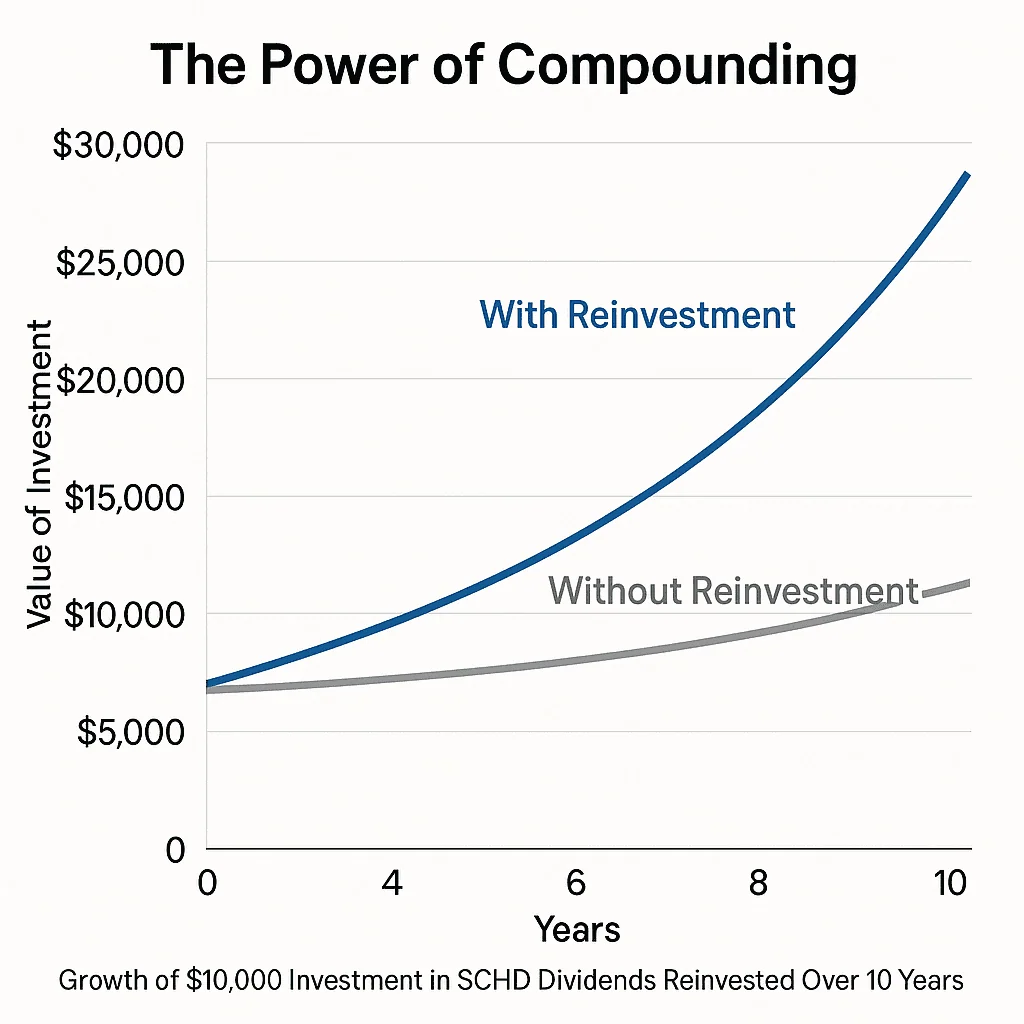

Example:

A $10,000 investment in SCHD with a 3.97% dividend yield reinvested via DRIP would be worth roughly $27,346 over ten years based on recent history. Manually doing it can achieve much the same result if consistently done, but will be behind the curve if cash lies around idle or is badly timed.

Tax Implications and Reporting for SCHD Dividend Reinvestment

Taxation of Reinvested Dividends

- All of the reinvestment SCHD dividends and cash are taxable in the same year they are received.

- Reinvested dividends are posted from IRS Form 1099-DIV as qualified or ordinary dividends, based on account type and holding period.

- In taxable accounts, you may be taxed even without receiving any cash dividend.

Strategies for Tax Efficiency

- Keep SCHD in tax-deferred accounts (IRAs, 401(k)s) to delay or avoid taxes on reinvested dividends.

- Keep a record of cost basis for every DRIP purchase, as every reinvestment forms a new tax lot.

- SCHD’s tax cost ratio over 10 years is approximately 1.02%, indicating the after-tax effect on long-term return. Forward planning can have you hold onto more of your profits.

If holding onto more of your returns is important to you, tax planning is also as important as choosing the right reinvestment option.

Optimizing Your SCHD Income Strategy: Actionable Tips and Tools

Choosing Between DRIP and Manual Reinvestment

- Use DRIP if you want maximum compounding with minimal effort and are focused on long-term SCHD accumulation.

- Opt for manual reinvestment if you want to:

- Time purchases for better value.

- Diversify or rebalance your portfolio.

- Use dividends for living expenses or other investments.

Tools and Calculators

To get realistic projections and scenario planning, go to this tool page for projecting SCHD income and comparing DRIP with manual reinvestment strategies. It’s not an officially approved Schwab tool, but it’s useful for whipping up what-ifs.

Most brokers will allow you to set DRIP on some holdings and take cash on others. Combine them together to suit your plan.

Advanced Strategies and Preventive Frameworks

Preventing Portfolio Imbalance

- Review your asset allocation periodically; DRIP will over-allocate to SCHD in the long term, particularly with its sector weightings (Consumer Staples and Energy each approximately 19%).

- Use manual reinvestment if you need strict portfolio targets or diversify your holdings.

Managing Tax Liabilities

- Monitor every reinvested dividend for precise cost basis and tax reporting.

- Get professional tax assistance for more complex situations, especially if you are investing in SCHD in taxable and tax-advantaged accounts.

If you are adventurous, you can even invest in undervalued segments of SCHD on a manual reinvestment or employ a core-satellite approach to mix DRIP with manual ones.

Dividend reinvestment, manual or automatic (DRIP) is an excellent method for accumulating SCHD income and compounding wealth. DRIP provides convenience and compounding, yet manual reinvestment offers flexibility and options. As brokerages continue to boost DRIP capabilities and fractional share arrangements, investors today can do more than ever before to tailor dividend approaches to their objectives. First, activate DRIP in your brokerage to auto-compound, or create a systematic manual reinvestment strategy that is in line with your overall investment goals. Periodically inspect your plan to optimize tax efficiency, portfolio alignment, and changing financial requirements to maximize SCHD dividend reinvestment’s long-term value.